Mastering the Nigeria Tax Act 2025: How to Protect Your ₦15 Million Assets from Avoidable Charges

The Nigeria Tax Act 2025 introduces a unified fiscal framework that fundamentally changes how individuals and businesses handle large transfers. This guide provides expert insights into navigating the ₦50 EMTL, distinguishing between taxable grants and tax-free gifts, and preparing dispute-proof documentation for the FIRS.

Nigeria’s New Fiscal Era: What You Need to Know

As the sun sets on the era of fragmented tax laws, the Nigeria Tax Act 2025 (Act No. 7) stands as the new constitution for wealth and commerce in Nigeria. Scheduled for full commencement on January 1, 2026, this Act consolidates everything from personal income tax to the Electronic Money Transfer Levy (EMTL). For many Nigerians handling sums between ₦5 million and ₦15 million, the question is no longer just about making money—it’s about keeping it without falling into a tax litigation trap.

The ₦15 Million Question: Withdrawals and Deposits

One of the most common points of confusion is whether moving your own money triggers a tax charge. Under the new law, a cash withdrawal of ₦5 million is not subject to tax or the EMTL. However, the ₦15 million deposit scenario is trickier. If you deposit ₦15 million into your own account at a different bank, you will be charged a fixed EMTL of ₦50.

Why? The Act applies a ₦50 levy to every electronic receipt of ₦10,000 and above, and only "intra-bank self-transfers" (same owner, same bank) are exempt. While ₦50 is nominal, the larger risk is the "Income Tax" flagging. Large credits of ₦5 million for individuals or ₦10 million for corporates are automatically reported to the authorities under anti-money laundering protocols. Without proof that this ₦15 million is your existing capital, the FIRS may flag it as "unreported business income".

Grants vs. Gifts: A Technical Minefield

Many entrepreneurs receive grants from organizations and hope to claim them as "gifts" to avoid the graduated income tax rates, which can reach 25% for high earners. Technically, this is an extremely high-risk move. Under Section 4(1)(h), "grants" are explicitly listed as taxable income.

While personal gifts (like a wedding gift from a relative) are generally not chargeable gains, an organization—as a legal entity—rarely has the "natural love and affection" required for a tax-exempt gift. If you attempt to reclassify a grant as a gift, the FIRS can use Section 191 (Artificial Transactions) to disregard the label and tax the full amount, adding heavy penalties.

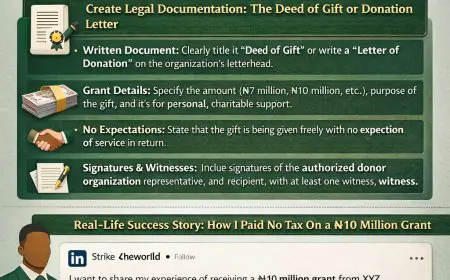

The "Dispute-Proof" Deed of Gift

If you are receiving a genuine personal gift of ₦15 million, a simple WhatsApp message saying "Gift" won't suffice. To protect yourself, you must prepare a formal Deed of Gift. This legal document must state that the donor receives "no consideration" (no goods or services) in return. Crucially, the document must be stamped; under Section 127, an unstamped document is generally not admissible as evidence in a tax dispute or court.

Filing and Management: Do You Need a Manager?

The FIRS does not typically "order" your income tax directly from your bank account unless you are in default. Instead, you must participate in the Self-Assessment system. The "Year of Assessment" follows the calendar year (Jan 1–Dec 31), and you must file your returns annually. While you are legally allowed to file yourself, complex scenarios involving multiple income streams or large grants usually require a tax manager to ensure you maximize legitimate deductions, such as business expenses or R&D credits.

Real-Life Case: The ₦15M "Tax-Free" Trap

Consider the story of "Chidi," an entrepreneur who received a ₦15 million "Innovation Grant." Chidi tried to file it as a personal gift to save on tax. Months later, he received an inquiry from the FIRS. Because the "gift" came from a commercial foundation and lacked a project report-free agreement, the FIRS applied Section 191. They taxed the full amount as business profit and added a 10% penalty. Chidi learned the hard way that substance always overrules description. For more guidance on official compliance, always refer to the FIRS Official Portal or the National Bureau of Statistics for economic updates.